50/30/20 Rule: The Simple Formula for Smart Budgeting

Managing your finances doesn’t have to be complicated. The 50/30/20 Rule is a simple, effective budgeting method that helps you allocate your income toward needs, wants, and savings. Whether you’re new to budgeting or looking for a better way to manage your money, the 50/30/20 Rule can provide clarity and structure to your financial life. In this guide, we’ll break down how the 50/30/20 Rule works, its benefits, and how you can apply it to achieve your financial goals.

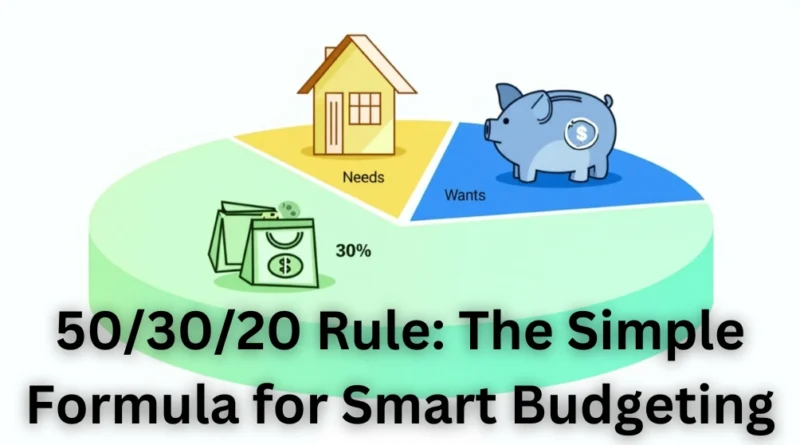

What Is the 50/30/20 Rule?

The 50/30/20 Rule is a budgeting framework that divides your after-tax income into three categories:

- 50% for Needs: Essential expenses like housing, utilities, groceries, and transportation.

- 30% for Wants: Non-essential expenses like dining out, entertainment, and hobbies.

- 20% for Savings and Debt Repayment: Building savings, paying off debt, and investing for the future.

This rule provides a balanced approach to budgeting, ensuring you cover your essential expenses while still enjoying life and preparing for the future.

Why Use the 50/30/20 Rule?

The 50/30/20 Rule is popular for several reasons:

- Simplicity: It’s easy to understand and implement, even for beginners.

- Flexibility: It allows for personalization based on your income and lifestyle.

- Balance: It ensures you’re meeting your needs, enjoying your wants, and saving for the future.

- Financial Awareness: It helps you track your spending and identify areas for improvement.

How to Apply the 50/30/20 Rule

Ready to start using the 50/30/20 Rule? Follow these steps to create a budget that works for you:

1. Calculate Your After-Tax Income

Start by determining your monthly after-tax income. This is the amount you take home after deductions like taxes, Social Security, and retirement contributions.

2. Divide Your Income into Categories

Using the 50/30/20 Rule, allocate your income as follows:

- 50% for Needs: Essential expenses that you can’t live without.

- 30% for Wants: Discretionary spending that enhances your lifestyle.

- 20% for Savings and Debt Repayment: Building your financial future.

3. Identify Your Needs (50%)

Needs are expenses that are necessary for your basic living. Examples include:

- Rent or mortgage payments

- Utilities (electricity, water, internet)

- Groceries

- Transportation (gas, public transit)

- Insurance (health, car, home)

- Minimum debt payments

If your needs exceed 50% of your income, look for ways to reduce costs, such as downsizing your home or cutting utility usage.

4. Allocate for Wants (30%)

Wants are non-essential expenses that improve your quality of life. Examples include:

- Dining out

- Entertainment (movies, concerts, streaming services)

- Hobbies and subscriptions

- Travel and vacations

- Shopping and personal care

If your wants exceed 30%, consider cutting back on discretionary spending to stay within your budget.

5. Prioritize Savings and Debt Repayment (20%)

The final 20% should go toward securing your financial future. This includes:

- Emergency savings

- Retirement contributions (401(k), IRA)

- Paying off debt (credit cards, student loans)

- Investments

If you’re struggling to save 20%, start small and gradually increase your contributions over time.

Benefits of the 50/30/20 Rule

The 50/30/20 Rule offers several advantages for managing your finances:

- Clarity: It provides a clear framework for allocating your income.

- Balance: It ensures you’re meeting your needs, enjoying your wants, and saving for the future.

- Flexibility: It can be adjusted to fit your unique financial situation.

- Simplicity: It’s easy to understand and implement, even for budgeting beginners.

Tips for Success with the 50/30/20 Rule

To make the most of the 50/30/20 Rule, follow these tips:

- Track Your Spending: Use budgeting apps or spreadsheets to monitor your expenses and stay on track.

- Automate Savings: Set up automatic transfers to your savings and retirement accounts.

- Adjust as Needed: Life changes, and so should your budget. Regularly review and adjust your allocations.

- Be Realistic: Don’t be too restrictive with your wants. Allow yourself some flexibility to enjoy life.

- Celebrate Milestones: Reward yourself for sticking to your budget and achieving financial goals.

Common Mistakes to Avoid with the 50/30/20 Rule

Even with the best intentions, it’s easy to make mistakes when using the 50/30/20 Rule. Here are some common pitfalls to avoid:

- Ignoring Irregular Expenses: Don’t forget to budget for occasional expenses like car repairs or holiday gifts.

- Overestimating Wants: Be honest about what qualifies as a want versus a need.

- Skipping Savings: Prioritize your savings and debt repayment, even if it means cutting back on wants.

- Not Tracking Progress: Regularly review your budget to ensure you’re staying on track.

- Being Too Rigid: Allow some flexibility in your budget to accommodate unexpected expenses or changes in income.

How to Adjust the 50/30/20 Rule for Your Needs

While the 50/30/20 Rule is a great starting point, it’s not one-size-fits-all. Here’s how to adjust it based on your financial situation:

- High Debt: If you have significant debt, consider allocating more than 20% to debt repayment.

- Low Income: If your income is limited, you may need to reduce your wants or find ways to lower your needs.

- High Savings Goals: If you’re saving for a big purchase or early retirement, increase your savings percentage.

- Variable Income: If your income fluctuates, base your budget on your average monthly income.

The Long-Term Impact of the 50/30/20 Rule

Using the 50/30/20 Rule consistently can have a lasting impact on your financial health:

- Debt Reduction: Prioritizing debt repayment helps you become debt-free faster.

- Wealth Building: Regular savings and investments grow your wealth over time.

- Financial Security: Building an emergency fund provides a safety net for unexpected expenses.

- Peace of Mind: Knowing you’re in control of your finances reduces stress and anxiety.

Conclusion

The 50/30/20 Rule is a simple yet powerful tool for managing your money and achieving your financial goals. By allocating your income toward needs, wants, and savings, you can create a balanced budget that works for your lifestyle. Whether you’re new to budgeting or looking for a better way to manage your finances, the 50/30/20 Rule is a great place to start. Ready to take control of your finances? Start using the 50/30/20 Rule today and build a brighter financial future!